‘The Russian invasion of Ukraine has put an end to the globalization we have experienced over the last three decades’. Thus spoke Larry Fink, CEO of BlackRock, the biggest investment firm in the world which manages $10 trillion in assets. Assuming the situation doesn’t spiral out of control – crossing our fingers and ‘touching iron’ in Italy, wood in Anglo-Saxon countries – this is likely to be one of the longer-lasting outcomes of the war (even if, at present, the picture looks rather different from the wreckage of the European battlefield).

That doesn’t mean the world will immediately revert to regional economies, customs barriers and restrictions on freedom of capital. Globalization implies a material infrastructure far too massive – Cyclopean, even – to be dismantled with such ease. A glance at container ports such as Busan or Rotterdam is enough to confirm this. Even better: take a look at MarineTraffic, a site that visualizes all vessels at sea anywhere in the world at any given moment. The volume is truly staggering.

But we should not underestimate what’s happening to the global economy and, above all, to finance. For the current war is not just asymmetric; it is also hybrid, in that it’s being fought on several different chessboards with diverse arsenals. On the one hand there’s Russia, waging a conventional war against Ukraine with tanks, missiles and bombs; but its true adversary is NATO, and ultimately the United States. On the other we have the US, conducting a proxy-conventional war against Russia, and preparing for a guerrilla war in the event that Ukraine is partially or totally annexed, while simultaneously launching a total and direct economic-financial blockade. It’s not by chance that the French finance minister Bruno Le Maire called exclusion from SWIFT a ‘financial nuclear weapon’.

The problem with nuclear weapons, however – be they literal or financial – is that they create radioactive fallout (I’ve recently written for Sidecar on the use and abuse of sanctions as an imperial instrument). In this case, what has been damaged is faith in globalization itself, and hence the very foundation on which it’s built. A globalized economy rests on the assumption that its overall order is more important than the contingencies of individual states. Capital can only move freely between banks in different nations if it is equally secure in any given institution. As such, globalization is based on the conviction that there are no national elites, but rather a single, global one that is invulnerable to the vicissitudes of state politics. This is a promise that enticed the rich in subject countries which hitherto felt subordinate to the imperial core. It presented these provincial elites with a mirage: the end of their subservience, their assimilation into the only dominating force on the planet. Under the regime of globalization, a magnate of any country that buys a house in London or opens a bank account in New York could expect their assets to be secure, irrespective of the fluctuations of global diplomacy. The slogan was ‘billionaires of the world unite’ (under a single transnational homeland): an illusion that has since been exposed by the Ukraine crisis.

If the United Kingdom goes about sequestering the property of Russian billionaires, why would other foreign magnates invest their capital in Belgravia, knowing that it might be targeted should their country fall out of favour with the United States? The billionaires of the world are realizing the falsity of their assumption that money doesn’t smell; under certain circumstances, certain people’s money does smell, badly. The seizure of Russia’s foreign reserves has been even more seismic. As Adam Tooze writes in the New Statesman, ‘The freezing of Russia’s central bank reserves means crossing the Rubicon. It brings conflict to the heart of the international monetary system. If the central bank reserves of a G20 member entrusted to the accounts of another G20 central bank are not sacrosanct, nothing in the financial world is.’ In short, the war has wounded globalization by prompting a loss of faith in the primacy of finance over politics – along with the material problems of provisioning, supply chains and raw materials.

It’s no coincidence that China’s ruling class are the most nervous about such issues. The Chinese deputy foreign minister Le Yucheng’s intervention, at a forum held at Tsinghua University one month after the Russian invasion, was illuminating in this regard. His firmest warning was that

globalization should not be ‘weaponized’…China has all along opposed unilateral sanctions that have neither basis in international law nor mandate of the Security Council. History has shown time and again that instead of solving problems, imposing sanctions is like ‘putting out fire with firewood’ and will only make things worse. Globalization is used as a weapon, and even people from the sports, cultural, art and entertainment communities are not spared. The abuse of sanctions will bring catastrophic consequences for the entire world.

No wonder China fashions itself as a paladin of globalization. It was the latter that, in the space of thirty years, turned China into the world’s second largest economic and military power. Any attempt to contain China implies a reversal of this trend, or at least its modification. (Contrary to received wisdom, there isn’t just one possible form globalization can take, but many; it can be structured in diverse ways, according to different configurations of power).

The election of Donald Trump marked a turning point in this bid to stifle China and, in tandem, decelerate globalization. Yet that election must be understood as part of a wider process, in which the cumulative effect of various events signalled a shift in global equilibria. Over the past six years, we have witnessed a series of ‘decouplings’ of global interfaces and untying of transnational nodes. Trump’s presidency, preceded by Brexit, was followed by the Covid-19 pandemic and the war in Ukraine. In each case, an aspect of globalization was thrown into question. Brexit halted European integration into the global financial markets based in London. With Trump, commercial wars – previously considered a relic of the past – were reignited. Then Covid interrupted crucial supply chains; now, the Ukrainian conflict has convulsed the geography of raw material provision, with the impact of the financial nuclear weapon still to be assessed.

The strategic debate within the US on how China ought to be confronted had already been sparked in the aftermath of the 2008 crisis, and continued throughout Obama’s tenure. Among American policymakers there was no univocal response to China’s rise, no ‘masterplan of capital’ that would have pleased the orthodox Marxists of old. In fact, ever since the question’s emergence, there have been pro- and anti-globalist factions, both of whom acknowledge that deglobalization could harm the interests of many powerful economic agents and trigger processes whose effects are difficult to calculate.

But if Trump’s election prompted American elites to reconsider the global order, it was the pandemic that revealed the compromised character of Chinese globalization. It is not frequently noted that, for over two years, Covid-19 was used to justify the complete closure of China to the outside world: a sealing off which hadn’t occurred since the Qing dynasty attempted to block the importation of opium in the 1830s. The complete disappearance of Chinese tourists from other countries was only its most visible expression. From a certain perspective, Covid was the vehicle for the (at least partial) reorientation of China’s economy towards internal consumption; though here too, it merely highlighted a tendency that had begun before Trump’s election.

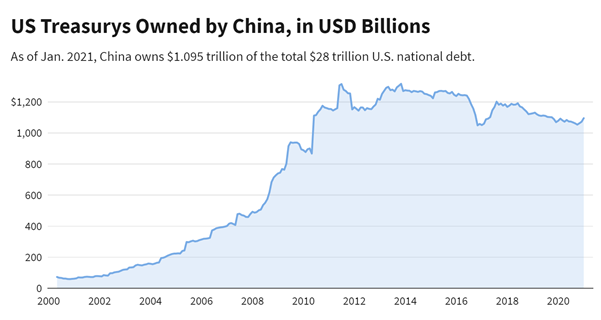

Globalization, the Chinese trade surplus and the American deficit are often folded together in a semi-mythic narrative. The story goes that China uses part of its surplus to buy US Treasury bonds in order to finance directly the US’s trade deficit – that is to say, American shopping in China. The graph below shows that this was substantially true until 2011 (indeed, we see an exponential increase in the Chinese Central Bank’s acquisition of US treasuries in the early 2000s). Yet the tale is interrupted in 2012. From then on, the amount of federal bonds held by Beijing has not increased – if anything, it has slowly diminished. Even as it continues to accrue an enormous yearly trade surplus, China has stopped buying new American bonds, only partially renewing those it already possesses.

Almost a quarter ($7.6 trillion) of US public debt is held by other countries, but contrary to popular belief, the largest holder of American debt isn’t China ($1.095 trillion in January 2022), but Japan ($1.3 trillion). Nor are oil-producing states such as Saudi Arabia and the UAE great acquirers of federal bonds; quite the opposite. Even more significant are the disproportionate amounts held by Luxembourg ($311 billion), Switzerland ($299 billion) and the Cayman Islands ($271 billion). This indicates supranational entities buying up US debt from their own accounts in tax havens (though one must note that in the last year the US has mainly charged Britain, France and Canada). By comparison, foreigners owned about 11% of Chinese government bonds as of January, a quarter of which was in the hands of Russia. Anxieties over Washington’s freezing of Russian reserves were immediately reflected in the value of US bonds, which suffered their worst month in February with the raising of interest rates linked to sales (or non-renewals). Chinese commentators were immediately worried about the country’s US reserves, fearing that in the long run – if conflict with the Americans escalated – they would meet the same fate as Russia’s.

A monetary storm is unlikely. What will follow, as we can see from the graph above, will be a gradual tightening of the belt with few sudden jolts, so as not to provoke the collapse of the dollar (or the revaluation of the renminbi). Yet fractures in global financial relations remain, as if the fabric of globalization has been lacerated. The best symbol of this is the elaborate ritual developing around the G20 summit, scheduled to take place in autumn on the island of Bali. Just to rub salt in the wound, Putin has floated the idea of attending, sowing panic among the NATO G20 members who would have to either tolerate his presence or expel him, risking the opposition and quite possibly the withdrawal of other countries such as India and Saudi Arabia (remember that those who abstained on the UN motion to condemn Russia included China, India, Saudi Arabia, the United Arab Emirates, Pakistan and 14 African countries, including South Africa). ‘No member has the right to remove another country as a member’, the Chinese Ministry of Foreign Affairs has affirmed, ‘the G20 should implement real multilateralism, strengthen unity and cooperation.’

Russia’s exclusion from the G20 would only be possible were it accompanied by expulsion from the World Trade Organization. But this would mean the death of globalization as we’ve come to know it. Evidently, none of the great powers is ready for this kind of dissolution. The US seems increasingly uncertain about deglobalization, as a nostalgic article in Foreign Affairs, ‘The End of Globalization?’, recently suggested. Let’s not forget that Biden faces midterm elections in November, and risks an unprecedented debacle (and a revolt in his own party) if he goes into them with runaway inflation and skyrocketing fuel prices.

The problem nobody seems capable of resolving is the superimposition of different temporal horizons: months of fighting in Ukraine; years of fallout from sanctions; and decades of a new world order (in which the eventual role of Russia remains a mystery, with or without Putin). What is certain is that the Chinese government is taking every precaution to avoid being hit by the unravelling of globalization, knowing full well that they – far more than Russia – are the real target of the US. After the phone call between Biden and Xi on 18 March, an anchor on Chinese state television mockingly paraphrased the former’s request to China: ‘Can you help me fight your friend so that I can concentrate on fighting you later?’

Read on: Fredric Jameson: ‘Globalization and Political Strategy’, NLR 4.