It has become a staple of conventional wisdom that global economic power is shifting inexorably towards the East and the South. Many insist that we are on the brink of a world-historic rebalancing that will result in the end of Western domination and the rise of a new hegemony. In particular, the emergence of China on the world stage—or re-emergence, if one has a longer time-scale in mind—is seen as heralding the dawn of an ‘Asian Century’. Yet this narrative of Western decline is misleading, above all because it greatly exaggerates the fading of the us as the world’s leading capitalist power. In fact, the contemporary rise of so-called ‘emerging markets’ poses even less of a challenge to us leadership than the revival of Western Europe and Japan in the post-war decades. There is already evidence to suggest that the growth rates of these markets may have peaked around 2011, without altering their basic dependence on commodity exports to Western economies (with the partial exception of China). The road towards convergence between the West and the Rest is a great deal rockier than most commentators believe, and there is no certainty about the outcome.

For the most part, debates on these questions lack a solid empirical foundation. Many of the scholars who conduct serious research in this area are hampered by a methodology that has become anachronistic in the age of global capitalism, one that equates national power with national accounts—gdp above all, but also balances of trade and payments, shares of world manufacturing and so on—as if we still lived in a world of nationally discrete political economies. Whether or not the equation ‘gdp = power’ was meaningful in the 1950s, the globalization of capital in recent decades has clearly rendered it problematic. When a substantial, often growing proportion of economic activity within a country’s borders is directed by foreign capitalists, we need to rethink the way that we measure national power—which does not mean that the concept itself is now irrelevant, as some have argued, since power is still nationally organized and concentrated.

It is useful in this respect to compare the past rise of Japan with the present rise of China. When Japanese electronics and automobiles began flooding Western markets in the 1960s and 70s, this was reflected both in a rising Japanese trade surplus and gdp and in the strengthening of Japan’s major corporations, many of which became household names. China, meanwhile, has seen its trade accounts and gdp soar in the age of globalization, and has become the world’s biggest exporter of electronics since 2004. Yet this growth has not been matched by the emergence of Chinese firms as world leaders in the field. Ninety per cent of what China Customs classifies as high-technology exports is actually produced by foreign-owned companies.footnote1 Thus, while an increasing share of global manufacturing takes place in the prc, much of this production is controlled, directly or indirectly, by outside interests. The contrast with Japan’s earlier ascent is stark. Any survey of global economic power must therefore take account of this shift, which means focusing our attention on the world’s leading transnational corporations.

Rise of the BRICs

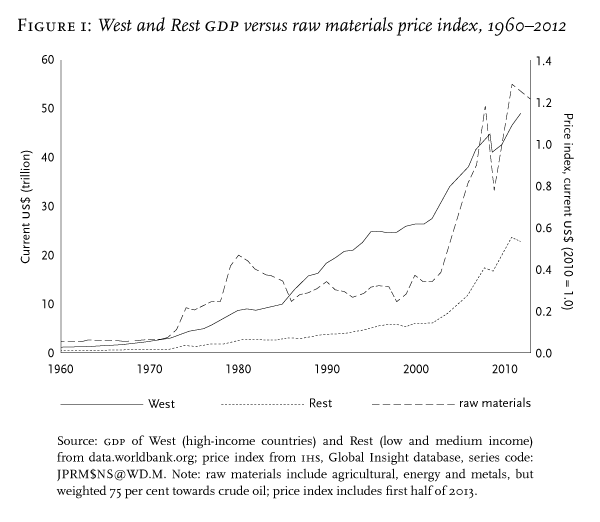

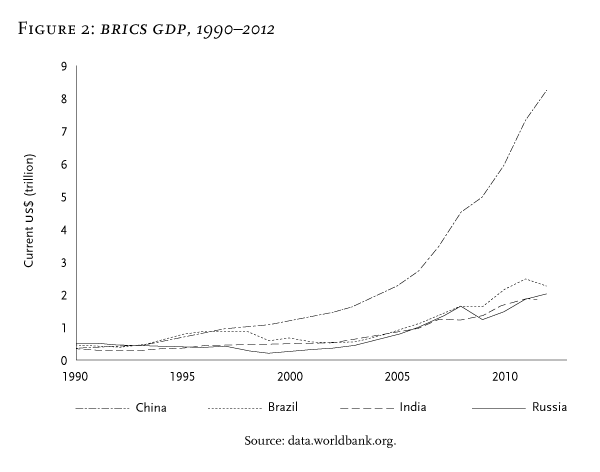

When we look carefully at the statistics, three salient points about the ‘rise of the Rest’ emerge. Firstly, much of that growth is linked to the so-called ‘commodity super-cycle’ that began in the early 2000s (Figure 1). Most analysts in the Anglo-American business press do not expect this unprecedented, exponential hike in prices—379 per cent from 2002 to 2011—to continue into the second decade of the new century. This has ominous implications for most of these countries, as they have been unable to escape from commodity-export dependence.footnote2 Secondly, four states account for the great bulk of the progress made by the Rest. Brazil, Russia, India and China produced 47 per cent of the Rest’s gdp in 2002 and 63 per cent in 2012. Hence, despite the (often fickle) attention lavished on many emerging markets by the business press as they seek opportunities for Western investors—from Chile to Indonesia, Turkey to Vietnam—when we seek to quantify the shifting balance of global capitalism, the brics are the only serious contenders. Finally, as Figure 2 demonstrates, China is by far the most significant player among these states: while they all had similar gdp levels in the early 90s, by 2012 China’s gdp was four times greater than that of any other bric.

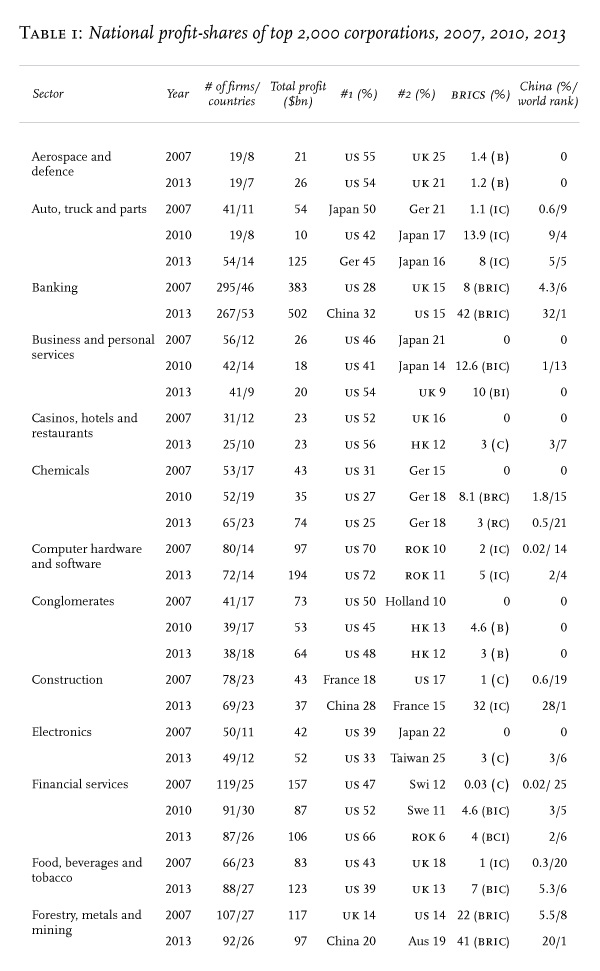

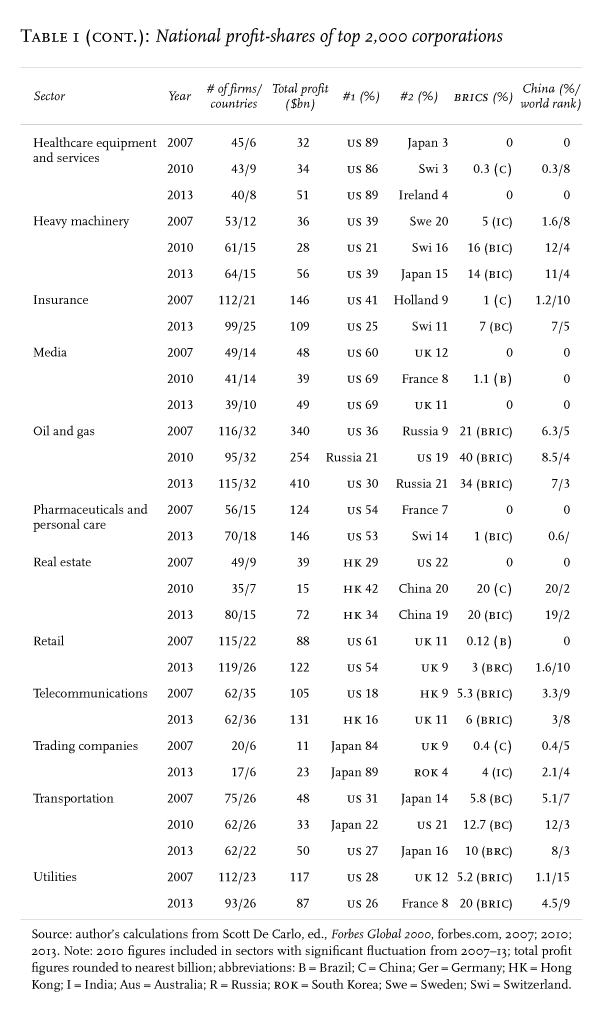

As we have noted, however, national accounts tell us very little about the structure of each political economy in a context of globalization: we need to dig much deeper. Table 1 (below) shows data compiled from the Forbes Global 2000 annual list of the world’s top 2,000 publicly traded companies, ranked by a composite of four metrics: assets, market value, profit and sales. These firms are organized into twenty-five broad sectors, with the number of firms and nationalities in each sector, as well as total profit, to aid with comparison (obviously, some sectors count for more than others). Table 1 also reveals the top two aggregate national profit-shares in each sector, in addition to the profit-shares of companies based in China and the other brics. In most sectors, data are given for two years, 2007 and 2013, while 2010 is also included when there is significant fluctuation. Therefore, we can observe in each sector changes from the last full year before the start of the financial crisis to the last year of available data at time of writing: seven crucial years during which the Rest were supposed to have risen at the expense of the West.

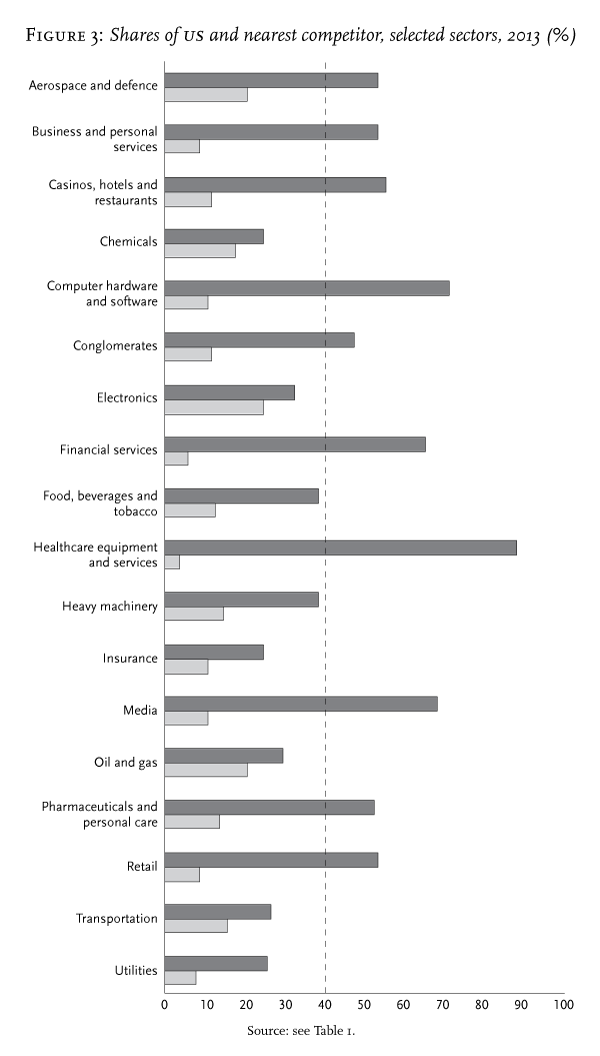

Before examining this data closely, we should ask in advance what the criteria for ‘dominance’ are. Most commentators agree, for example, that the us occupied a dominant position in the global economy during the 1950s, at a time when its share of world gdp was approximately 40 per cent. Does it follow that any proportion lower than 40 per cent cannot be regarded as ‘dominant’? It is also important to compare the leading share with its nearest competitor and consider the extent of its lead. If the us profit-share declines from 40 to 30 per cent in one sector, while that of the number two country declines from 20 to 10, can this really be said to represent ‘American decline’? In the first instance the American share is double its nearest competitor, in the second instance triple. Benchmarks for ‘decline’ and ‘dominance’ can thus be somewhat arbitrary.

The most striking feature of Table 1 may be the remarkable number of sectors in which American firms still held the lead by 2013: eighteen out of twenty-five. In fact, American leadership had increased in absolute terms across five sectors (business and personal services; casinos, hotels and restaurants; computer hardware and software; financial services; and media), and in relative terms—as a multiple of its nearest competitor—across a further five (aerospace and defence; food, beverages and tobacco; heavy machinery; retail; and utilities). In another five sectors, American leadership declined with the onset of the financial crisis, only to recover after 2010: these were conglomerates; healthcare equipment and services; heavy machinery; oil and gas; and transportation. Figure 3 (below) presents this data in graphic form, showing the gap between the us profit-share and that of its nearest competitors in 2013 in the eighteen sectors in which it held the lead. If we define 40 per cent as the benchmark for dominance, on the grounds set out above, American firms hold sway in ten sectors, especially those at the technological cutting edge: aerospace and defence; business and personal services; casinos, hotels and restaurants; computer hardware and software; conglomerates; financial services; healthcare equipment and services; media; pharmaceuticals and personal care; and retail.footnote3 The only other nations to dominate even a single sector are Germany in auto, truck and parts—note, however, the massive instability in this sector—and Japan in trading companies. On the other hand, American positions in the remaining ten sectors have declined, with no American presence in trading companies, a sector that accommodates an enterprise-type largely peculiar to Japan: the sogo shosha.

The number of sectors in which corporations domiciled in the brics have advanced their profit-shares during this period is also remarkable, however: twenty-two out of twenty-five.footnote4 There are six sectors in which the rise of the brics has been staggering: banking (from 8 per cent in 2007 to 42 per cent in 2013); construction (from 1 to 32 per cent); forestry, metals and mining (from 22 to 41 per cent); real estate (from zero to 20 per cent); utilities (from 5.2 to 20 per cent); and oil and gas (from 21 to 40 per cent in 2010, but then down to 34 per cent in 2013). Unsurprisingly, China accounts for much of the progress across the twenty-two sectors, most of all in banking (32 per cent), construction (28 per cent), and real estate (19 per cent). By contrast, the achievements of Brazil, Russia and India are concentrated in those sectors linked to the commodities super-cycle: namely forestry, metals and mining, and oil and gas, along with banking (as foreign exchange and profits from commodity exports are deposited in national banks).

Without sectoral diversification, these countries remain exposed to price fluctuations. Russia is the most vulnerable in this regard, as its economic revival has been almost entirely driven by rising fossil-fuel prices. India and Brazil have a scattering of industrial niches, the former in auto, truck and parts and computer hardware and software (both 3 per cent), the latter in aerospace and defence (1.2 per cent) and conglomerates (3 per cent). These minor footholds hardly threaten the United States, let alone the Western economies in general. China, on the other hand, now ranks in the global top five across twelve sectors: auto, truck and parts; banking; computer hardware and software; construction; forestry, metals and mining; heavy machinery; insurance; oil and gas; real estate; telecommunications (with China Mobile listed in Hong Kong but headquartered in China); trading companies; and transportation. These extraordinary advances are the real story behind the ‘rise of the Rest’.

Chinese challenges

Yet if we examine China’s progress more carefully, its newfound industrial strength may not be as impressive as appearances would suggest. The country’s political economy has a number of peculiar features. Public investment plays an exceptionally large role: the Chinese state channels funding via its top banks to construction, heavy industry and raw material producers, all of which are publicly owned, boosting the profits of these firms to world-leading heights. In 2008–09, Beijing responded to the global crisis by introducing a stimulus second only to that of the United States, further strengthening its state-owned enterprises (as can be observed in a number of sectors in Table 1). Many observers, however, including Communist Party elites in China itself, believe that this model is unsustainable, especially as Chinese debt continues to soar and over-capacity grips many sectors.footnote5 Whether China can shift the balance of its economy from state investment to domestic consumption without serious social upheaval—and without challenging the now deeply entrenched elite interests that stand behind the current growth model—is one of the great uncertainties in global capitalism today.footnote6 But in every conceivable scenario, from managed transition to collapse, the profits of soes linked to the investment-driven growth model will most likely decline over the next five years or so—and consequently their global rankings.

Another Chinese peculiarity lies in the following paradox: among the major economies, it is at once one of the most closed and most open to foreign capital. To be more precise, certain sectors are closed, inward-looking and predominantly state-owned, while others face in the opposite direction, with a mix of state and private enterprises, both foreign and domestic. This two-tier structure explains why Chinese firms lead in certain areas while they lag far behind in others. China surpassed the us in 2011 to become the world’s largest pc market, yet the Chinese profit-share in computer hardware and software is a measly 2 per cent—barely discernible when set against the American share of 72 per cent. And despite also becoming the world’s largest automobile market in 2009, its profit-share in auto, truck and parts remains stuck at 5 per cent, while the ‘Big Three’ nationalities—Germany, Japan and the us—gobble up more than half of the profits in this sector. Even in China itself, foreign firms have a combined market share in excess of 70 per cent, with Volkswagen and General Motors the dominant players.footnote7 Two decades of large-scale investment by the Chinese state in its auto industry have thus far ended in failure.

This is not the only sector in which Western—especially us—firms dominate the Chinese terrain: Pepsi and Coca-Cola account for 87 per cent of Chinese soft drink sales; Google Android has obliterated competition from rival smartphone operating systems, increasing its market share from 0.6 per cent in 2009 to 86.4 per cent in 2012; and Wal-Mart controls 8 per cent of the Chinese retail trade—easily the largest portion of a highly fragmented market, with over half a million firms jockeying for position. Boeing alone supplies more than half of China’s commercial aircraft fleet.footnote8 As a result, many American firms are in a strong position to benefit if China does succeed in redirecting its growth model towards domestic consumption.

As we noted earlier, China has been the world’s biggest exporter of electronics since 2004, including computer hardware. Yet its profit-share in the electronics sector is just 3 per cent—no match for Taiwan’s 25 per cent, let alone the 33 per cent accruing to us companies. The case of Hon Hai Precision Industry shows how limited national accounts can be as a measure of power in the age of globalization. Through its wholly owned subsidiary Foxconn, Hon Hai is China’s largest private employer—with more than a million workers on its payroll—and its biggest exporter; it is also the world’s leading contract manufacturer for the electronics industry. The company performs final assembly for a range of high-tech firms, from Cisco, Dell and Hewlett-Packard to Microsoft, Sony and Nintendo—not forgetting Apple’s iPads and iPhones, the vast majority of which are assembled by Foxconn plants. Its own profits for 2013, however, were ‘only’ $10.7 billion; one-quarter of Apple’s, and a tiny fraction of the combined profits earned by the Western and Japanese companies whose products it assembles. It is easy to discern why. In 2010, components of the iPhone 3 cost Apple $172.46 (two-thirds going to Japan’s Toshiba, Germany’s Infineon and South Korea’s Samsung), while final assembly cost the firm just $6.50 (all of which went to Foxconn).footnote9 Depending on the retail price, Apple’s profit on each phone could be hundreds of dollars. This commanding position stems from the American firm’s control over the global supply chain and its ownership of the highest value ‘modules’ (brand, marketing, innovation, research and development). Contract manufacturers like Hon Hai struggle to climb up the value chain as their competitive edge derives largely from cost-cutting, reducing their ability to take the risks involved in developing their own branded designs and global marketing campaigns.footnote10 Furthermore, control of Hon Hai itself does not lie in Chinese hands: it was founded by the Taiwanese billionaire Terry Gou, who is still its largest shareholder. It thus remains far from certain that China can match the performance of Taiwanese or Korean high-tech firms, never mind the American market leaders. According to China Customs figures from 2010, three-quarters of the prc’s top 200 exporting companies are foreign-owned.footnote11

Ownership and innovation

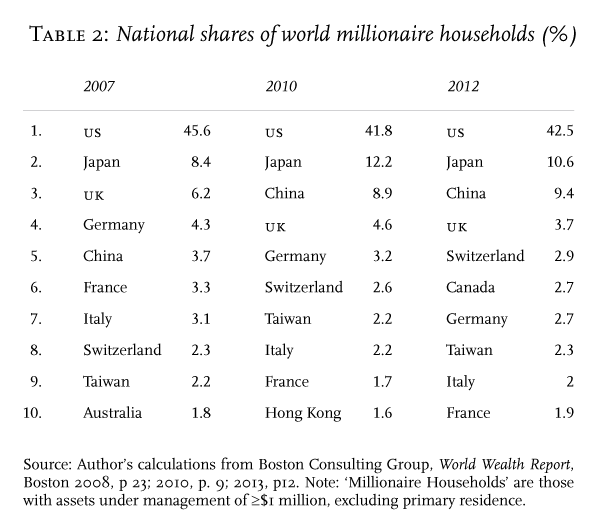

While it is clear from what has been said above that us corporations still occupy the commanding heights of global capitalism, this invites a further question: who owns those corporations? Another debate arising from the globalization of capital concerns the possible emergence of a ‘trans-national capitalist class’ (tcc). If we assume that the ownership of us companies is globally dispersed, in what sense can the health of those companies be said to represent ‘American power’? I shall confine myself to addressing one aspect of this controversy: the supposed dispersion of ownership, which provides the ultimate rationale for most of those who argue that a tcc has now come into being.footnote12 According to my calculations from the Bloomberg Professional database, in July 2013 the average American ownership of the top 100 us corporations—as ranked by Forbes—was 85 per cent. The nature of the biggest shareholders varies considerably from one firm to the next, encompassing individuals and family trusts, investment funds and other wealth managers. Among the latter, just 2 per cent of the assets managed by us financial services companies came from investors with no legal residence or tax domicile in the country.footnote13 Since American corporations, which are largely owned by us residents, lead the way in so many different sectors, it should come as no surprise that by far the greatest portion of the world’s millionaires come from the United States (Table 2). China is the only country among the Rest with a significant (and growing) national share, challenging Japan’s no. 2 spot in 2012.footnote14

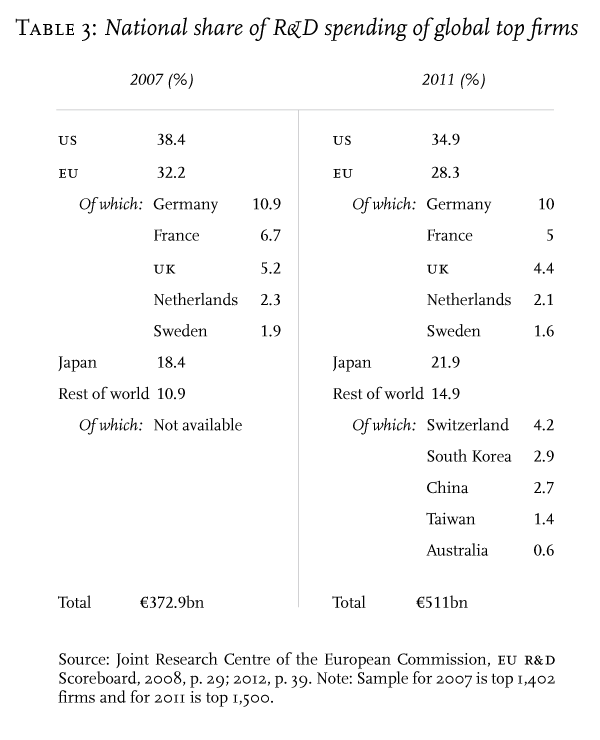

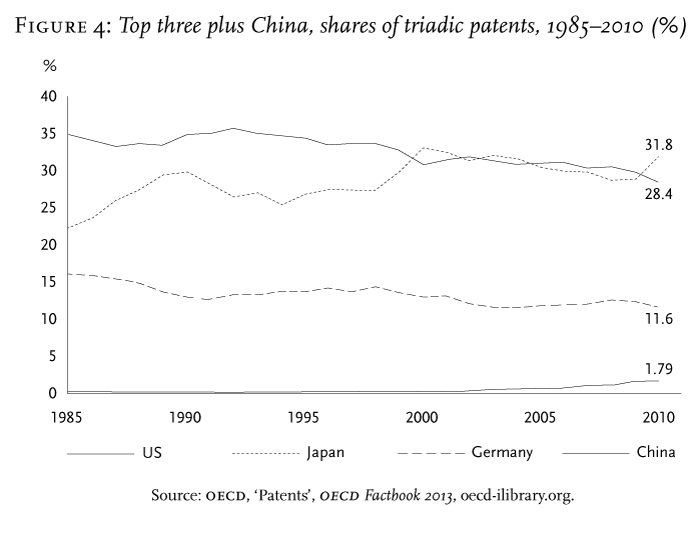

If we wish to identify future trends in the distribution of global economic power, one important factor to consider is whether the balance of innovation is shifting from the West to the Rest. Table 3 shows the national shares of r&d spending among the world’s top 1,402 firms in 2007 and the top 1,500 in 2011.footnote15 While the American share declined, Japan’s increased, ensuring that the two countries together accounted for the same proportion—56.8 per cent—in both 2007 and 2011. Hence, even if the ‘Rest of the World’ (a category which includes South Korea, Australia and Switzerland) has expanded its share from 10.9 to 14.9 per cent in the same period—with China now occupying third place among this group of countries—it is very unlikely that the technological leadership of Japan and the United States will be challenged in the near future. Figure 4 (opposite) takes a longer view, across a twenty-five year timescale, using triadic patents as a proxy for innovation.footnote16 Japan and the us generated 60 per cent of patents in 2010, and while China has made real advances in this field—from 0.46 per cent in 2004 to 1.79 per cent in 2010—it has a long way to travel before we can speak of any meaningful convergence between the Chinese economy and its more advanced rivals.

Global prospects

The findings presented above illuminate three aspects of today’s global capitalist system: the continued dominance of the us, the extraordinary rise of the Rest (China in particular), and the tight correlation between that rise and the raw materials price index. Most commentary focuses on the second aspect, wrongly assuming that it comes at the expense of the first. Yet American companies have the leading profit-shares among the world’s top 2,000 firms in eighteen of twenty-five sectors, and a dominant position in ten—especially those at the technological frontier. In a reflection of this global hegemony, two-fifths of the world’s millionaire households are American. The declining us share of global gdp—from 40 per cent in the 1950s to 22 per cent in 2012—would not have led us to anticipate such figures. It is therefore essential to move beyond national accounts and study the world’s top corporations in order to get a sense of where economic power is really concentrated.

We can recognize the persistence of us economic hegemony without denying the remarkable expansion of the Rest—especially the brics—in twenty-two of the twenty-five sectors. However, China is the only country that can be described as a serious contender to join the advanced capitalist world, with its progress across a whole range of industries, and its position among the global top five in twelve sectors. While some emerging markets now have a presence in branches of the economy not linked to raw materials, none can boast China’s sectoral diversity. Yet even the prc lacks a substantial presence in a number of key areas, some of which are already dominated by foreign firms in the country itself. We have discussed structural barriers to further Chinese progress, stemming from its investment- and export-driven growth model. Of course, there are also social and environmental constraints, demography and the hukou system foremost among them.footnote17

A slowdown of emerging markets is also to be expected, as the commodities super-cycle appears already to have peaked. This is not to say that the raw materials price index will collapse, or remain stuck at its current level. But it is unlikely to rise at the same rate as before, contrary to the assumptions of many forecasts made in the immediate wake of the global financial crisis. Analysts are now warning of the ‘middle-income trap’: the apparent glass ceiling faced by middle-income countries when they attempt to join the developed capitalist world.footnote18 Those with diversified political economies will have the best chance of escaping this slowdown. China is by far the most likely contender, yet faces significant challenges of its own. The leading role of us capital in the global economy is thus likely to endure for some time to come.