There is a widespread sense today that capitalism is in critical condition, more so than at any time since the end of the Second World War.footnote1 Looking back, the crash of 2008 was only the latest in a long sequence of political and economic disorders that began with the end of postwar prosperity in the mid-1970s. Successive crises have proved to be ever more severe, spreading more widely and rapidly through an increasingly interconnected global economy. Global inflation in the 1970s was followed by rising public debt in the 1980s, and fiscal consolidation in the 1990s was accompanied by a steep increase in private-sector indebtedness.footnote2 For four decades now, disequilibrium has more or less been the normal condition of the ‘advanced’ industrial world, at both the national and the global levels. In fact, with time, the crises of postwar oecd capitalism have become so pervasive that they have increasingly been perceived as more than just economic in nature, resulting in a rediscovery of the older notion of a capitalist society—of capitalism as a social order and way of life, vitally dependent on the uninterrupted progress of private capital accumulation.

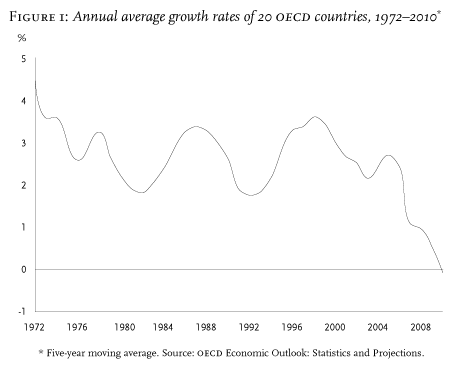

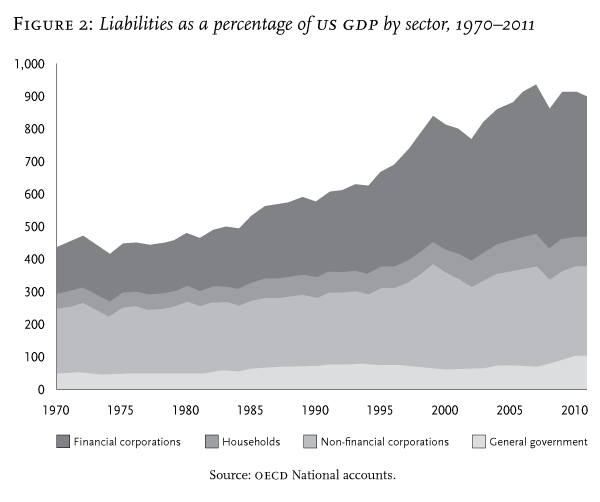

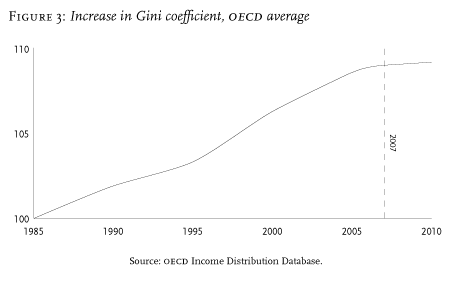

Crisis symptoms are many, but prominent among them are three long-term trends in the trajectories of rich, highly industrialized—or better, increasingly deindustrialized—capitalist countries. The first is a persistent decline in the rate of economic growth, recently aggravated by the events of 2008 (Figure 1, below). The second, associated with the first, is an equally persistent rise in overall indebtedness in leading capitalist states, where governments, private households and non-financial as well as financial firms have, over forty years, continued to pile up financial obligations (for the us, see Figure 2, below). Third, economic inequality, of both income and wealth, has been on the ascent for several decades now (Figure 3, below), alongside rising debt and declining growth.

Steady growth, sound money and a modicum of social equity, spreading some of the benefits of capitalism to those without capital, were long considered prerequisites for a capitalist political economy to command the legitimacy it needs. What must be most alarming from this perspective is that the three critical trends I have mentioned may be mutually reinforcing. There is mounting evidence that increasing inequality may be one of the causes of declining growth, as inequality both impedes improvements in productivity and weakens demand. Low growth, in turn, reinforces inequality by intensifying distributional conflict, making concessions to the poor more costly for the rich, and making the rich insist more than before on strict observance of the ‘Matthew principle’ governing free markets: ‘For unto every one that hath shall be given, and he shall have abundance: but from him that hath not shall be taken even that which he hath.’footnote3 Furthermore, rising debt, while failing to halt the decline of economic growth, compounds inequality through the structural changes associated with financialization—which in turn aimed to compensate wage earners and consumers for the growing income inequality caused by stagnant wages and cutbacks in public services.

Can what appears to be a vicious circle of harmful trends continue forever? Are there counterforces that might break it—and what will happen if they fail to materialize, as they have for almost four decades now? Historians inform us that crises are nothing new under capitalism, and may in fact be required for its longer-term health. But what they are talking about are cyclical movements or random shocks, after which capitalist economies can move into a new equilibrium, at least temporarily. What we are seeing today, however, appears in retrospect to be a continuous process of gradual decay, protracted but apparently all the more inexorable. Recovery from the occasional Reinigungskrise is one thing; interrupting a concatenation of intertwined, long-term trends quite another. Assuming that ever lower growth, ever higher inequality and ever rising debt are not indefinitely sustainable, and may together issue in a crisis that is systemic in nature—one whose character we have difficulty imagining—can we see signs of an impending reversal?

Another stopgap

Here the news is not good. Six years have passed since 2008, the culmination so far of the postwar crisis sequence. While memory of the abyss was still fresh, demands and blueprints for ‘reform’ to protect the world from a replay abounded. International conferences and summit meetings of all kinds followed hot on each other’s heels, but half a decade later hardly anything has come from them. In the meantime, the financial industry, where the disaster originated, has staged a full recovery: profits, dividends, salaries and bonuses are back where they were, while re-regulation became mired in international negotiations and domestic lobbying. Governments, first and foremost that of the United States, have remained firmly in the grip of the money-making industries. These, in turn, are being generously provided with cheap cash, created out of thin air on their behalf by their friends in the central banks—prominent among them the former Goldman Sachs man Mario Draghi at the helm of the ecb—money which they then sit on or invest in government debt. Growth remains anaemic, as do labour markets; unprecedented liquidity has failed to jumpstart the economy; and inequality is reaching ever more astonishing heights, as what little growth there is has been appropriated by the top one per cent of income earners—the lion’s share by a small fraction of them.footnote4

There would seem to be little reason indeed to be optimistic. For some time now, oecd capitalism has been kept going by liberal injections of fiat money, under a policy of monetary expansion whose architects know better than anyone else that it cannot continue forever. In fact, several attempts were made in 2013 to kick the habit, in Japan as well as in the us, but when stock prices plunged in response, ‘tapering’, as it came to be called, was postponed for the time being. In mid-June, the Bank for International Settlements (bis) in Basel—the mother of all central banks—declared that ‘quantitative easing’ must come to an end. In its Annual Report, the Bank pointed out that central banks had, in reaction to the crisis and the slow recovery, expanded their balance sheets, ‘which are now collectively at roughly three times their pre-crisis level—and rising’.footnote5 While this had been necessary to ‘prevent financial collapse’, now the goal had to be ‘to return still-sluggish economies to strong and sustainable growth’. This, however, was beyond the capacities of central banks, which:

cannot enact the structural economic and financial reforms needed to return economies to the real growth paths authorities and their publics both want and expect. What central-bank accommodation has done during the recovery is to borrow time . . . But the time has not been well used, as continued low interest rates and unconventional policies have made it easy for the private sector to postpone deleveraging, easy for the government to finance deficits, and easy for the authorities to delay needed reforms in the real economy and in the financial system. After all, cheap money makes it easier to borrow than to save, easier to spend than to tax, easier to remain the same than to change.

Apparently this view was shared even by the Federal Reserve under Bernanke. By the late summer of 2013, it seemed once more to be signalling that the time of easy money was coming to an end. In September, however, the expected return to higher interest rates was again put off. The reason given was that ‘the economy’ looked less ‘strong’ than was hoped. Global stock prices immediately went up. The real reason, of course, why a return to more conventional monetary policies is so difficult is one that an international institution like bis is freer to spell out than a—for the time being—more politically exposed national central bank. This is that as things stand, the only alternative to sustaining capitalism by means of an unlimited money supply is trying to revive it through neoliberal economic reform, as neatly encapsulated in the second subtitle of the bis’s 2012–13 Annual Report: ‘Enhancing Flexibility: A Key to Growth.’ In other words, bitter medicine for the many, combined with higher incentives for the few.footnote6

A problem with democracy

It is here that discussion of the crisis and the future of modern capitalism must turn to democratic politics. Capitalism and democracy had long been considered adversaries, until the postwar settlement seemed to have accomplished their reconciliation. Well into the twentieth century, owners of capital had been afraid of democratic majorities abolishing private property, while workers and their organizations expected capitalists to finance a return to authoritarian rule in defence of their privileges. Only in the Cold War world did capitalism and democracy seem to become aligned with one another, as economic progress made it possible for working-class majorities to accept a free-market, private-property regime, in turn making it appear that democratic freedom was inseparable from, and indeed depended on, the freedom of markets and profit-making. Today, however, doubts about the compatibility of a capitalist economy with a democratic polity have powerfully returned. Among ordinary people, there is now a pervasive sense that politics can no longer make a difference in their lives, as reflected in common perceptions of deadlock, incompetence and corruption among what seems an increasingly self-contained and self-serving political class, united in their claim that ‘there is no alternative’ to them and their policies. One result is declining electoral turnout combined with high voter volatility, producing ever greater electoral fragmentation, due to the rise of ‘populist’ protest parties, and pervasive government instability.footnote7

The legitimacy of postwar democracy was based on the premise that states had a capacity to intervene in markets and correct their outcomes in the interest of citizens. Decades of rising inequality have cast doubt on this, as has the impotence of governments before, during and after the crisis of 2008. In response to their growing irrelevance in a global market economy, governments and political parties in oecd democracies more or less happily looked on as the ‘democratic class struggle’ turned into post-democratic politainment.footnote8 In the meantime, the transformation of the capitalist political economy from postwar Keynesianism to neoliberal Hayekianism progressed smoothly: from a political formula for economic growth through redistribution from the top to the bottom, to one expecting growth through redistribution from the bottom to the top. Egalitarian democracy, regarded under Keynesianism as economically productive, is considered a drag on efficiency under contemporary Hayekianism, where growth is to derive from insulation of markets—and of the cumulative advantage they entail—against redistributive political distortions.

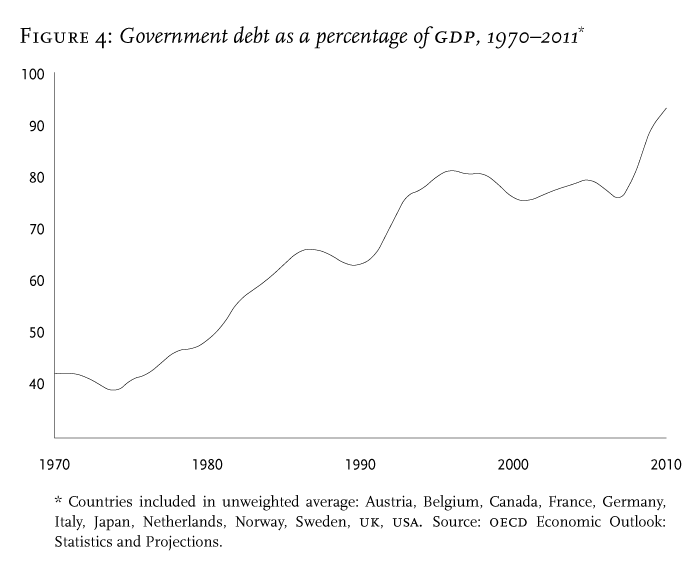

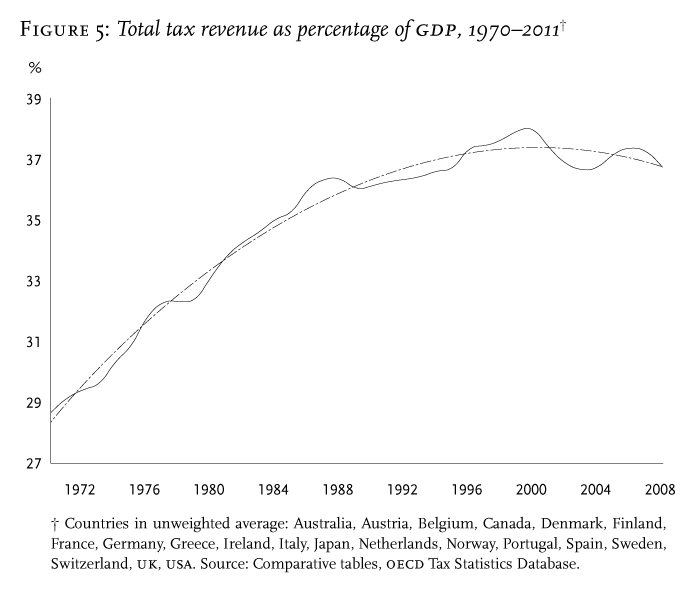

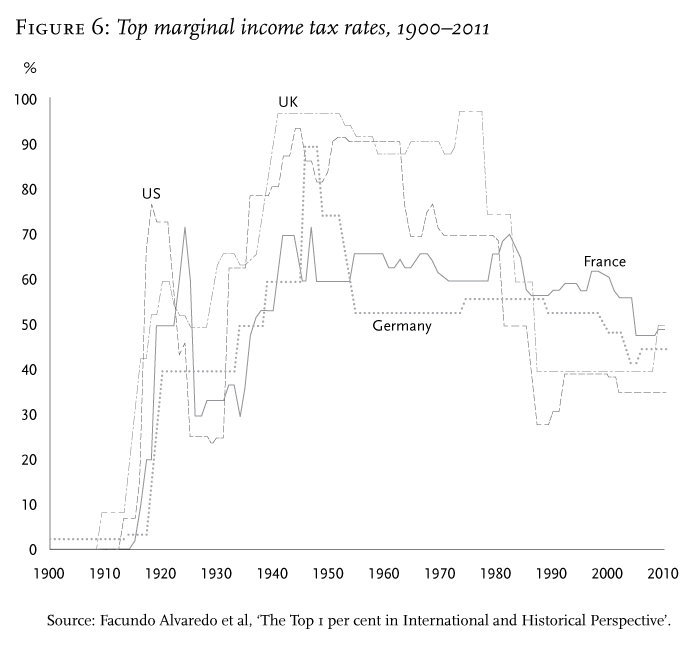

A central topic of current anti-democratic rhetoric is the fiscal crisis of the contemporary state, as reflected in the astonishing increase in public debt since the 1970s (Figure 4, below). Growing public indebtedness is put down to electoral majorities living beyond their means by exploiting their societies’ ‘common pool’, and to opportunistic politicians buying the support of myopic voters with money they do not have.footnote9 However, that the fiscal crisis was unlikely to have been caused by an excess of redistributive democracy can be seen from the fact that the buildup of government debt coincided with a decline in electoral participation, especially at the lower end of the income scale, and marched in lockstep with shrinking unionization, the disappearance of strikes, welfare-state cutbacks and exploding income inequality. What the deterioration of public finances was related to was declining overall levels of taxation (Figure 5) and the increasingly regressive character of tax systems, as a result of ‘reforms’ of top income and corporate tax rates (Figure 6). Moreover, by replacing tax revenue with debt, governments contributed further to inequality, in that they offered secure investment opportunities to those whose money they would or could no longer confiscate and had to borrow instead. Unlike taxpayers, buyers of government bonds continue to own what they pay to the state, and in fact collect interest on it, typically paid out of ever less progressive taxation; they can also pass it on to their children. Moreover, rising public debt can be and is being utilized politically to argue for cutbacks in state spending and for privatization of public services, further constraining redistributive democratic intervention in the capitalist economy.

Institutional protection of the market economy from democratic interference has advanced greatly in recent decades. Trade unions are on the decline everywhere and have in many countries been all but rooted out, especially in the us. Economic policy has widely been turned over to independent—i.e., democratically unaccountable—central banks concerned above all with the health and goodwill of financial markets.footnote10 In Europe, national economic policies, including wage-setting and budget-making, are increasingly governed by supranational agencies like the European Commission and the European Central Bank that lie beyond the reach of popular democracy. This effectively de-democratizes European capitalism—without, of course, de-politicizing it.

Still, doubts remain among the profit-dependent classes as to whether democracy will, even in its emasculated contemporary version, allow for the neoliberal ‘structural reforms’ necessary for their regime to recover. Like ordinary citizens, although for the opposite reasons, elites are losing faith in democratic government and its suitability for reshaping societies in line with market imperatives. Public Choice’s disparaging view of democratic politics as a corruption of market justice, in the service of opportunistic politicians and their clientele, has become common sense among elite publics—as has the belief that market capitalism cleansed of democratic politics will not only be more efficient but also virtuous and responsible.footnote11 Countries like China are complimented for their authoritarian political systems being so much better equipped than majoritarian democracy, with its egalitarian bent, to deal with what are claimed to be the challenges of ‘globalization’—a rhetoric that is beginning conspicuously to resemble the celebration by capitalist elites during the interwar years of German and Italian fascism (and even Stalinist communism) for their apparently superior economic governance.footnote12

For the time being, the neoliberal mainstream’s political utopia is a ‘market-conforming democracy’, devoid of market-correcting powers and supportive of ‘incentive-compatible’ redistribution from the bottom to the top.footnote13 Although that project is already far advanced in both Western Europe and the United States, its promoters continue to worry that the political institutions inherited from the postwar compromise may at some point be repossessed by popular majorities, in a last-minute effort to block progress toward a neoliberal solution to the crisis. Elite pressures for economic neutralization of egalitarian democracy therefore continue unabated; in Europe this takes the form of a continuing relocation of political-economic decision-making to supranational institutions such as the European Central Bank and summit meetings of government leaders.

Capitalism on the brink?

Has capitalism seen its day? In the 1980s, the idea that ‘modern capitalism’ could be run as a ‘mixed economy’, both technocratically managed and democratically controlled, was abandoned. Later, in the neoliberal revolution, social and economic order was reconceived as benevolently emerging from the ‘free play of market forces’. But with the crash of 2008, the promise of self-regulating markets attaining equilibrium on their own was discredited as well, without a plausible new formula for political-economic governance coming into view. This alone may be regarded as a symptom of a crisis that has become systemic, the more so the longer it lasts.

In my view it is high time, in the light of decades of declining growth, rising inequality and increasing indebtedness—as well as of the successive agonies of inflation, public debt and financial implosion since the 1970s—to think again about capitalism as a historical phenomenon, one that has not just a beginning, but also an end. For this, we need to part company with misleading models of social and institutional change. As long as we imagine the end of capitalism being decreed, Leninist-style, by some government or central committee, we cannot but consider capitalism eternal. (In fact it was communism, centralized as it was in Moscow, that could be and was terminated by decree.) Matters are different if, instead of imagining it being replaced by collective decision with some providentially designed new order, we allow for capitalism to collapse by itself.

I suggest that we learn to think about capitalism coming to an end without assuming responsibility for answering the question of what one proposes to put in its place. It is a Marxist—or better: modernist—prejudice that capitalism as a historical epoch will end only when a new, better society is in sight, and a revolutionary subject ready to implement it for the advancement of mankind. This presupposes a degree of political control over our common fate of which we cannot even dream after the destruction of collective agency, and indeed the hope for it, in the neoliberal-globalist revolution. Neither a utopian vision of an alternative future nor superhuman foresight should be required to validate the claim that capitalism is facing its Götterdämmerung. I am willing to make exactly this claim, although I am aware of how many times capitalism has been declared dead in the past. In fact, all of the main theorists of capitalism have predicted its impending expiry, ever since the concept came into use in the mid-1800s. This includes not just radical critics like Marx or Polanyi, but also bourgeois theorists such as Weber, Schumpeter, Sombart and Keynes.footnote14

That something has failed to happen, in spite of reasonable predictions that it would, does not mean that it will never happen; here, too, there is no inductive proof. I believe that this time is different, one symptom being that even capitalism’s master technicians have no clue today how to make the system whole again—see, for example, the recently published minutes of the deliberations of the Federal Reserve’s board in 2008,footnote15 or the desperate search of central bankers, mentioned above, for the right moment to end ‘quantitative easing’. This, however, is only the surface of the problem. Beneath it is the stark fact that capitalist progress has by now more or less destroyed any agency that could stabilize it by limiting it; the point being that the stability of capitalism as a socio-economic system depends on its Eigendynamik being contained by countervailing forces—by collective interests and institutions subjecting capital accumulation to social checks and balances. The implication is that capitalism may undermine itself by being too successful. I will argue this point in more detail below.

The image I have of the end of capitalism—an end that I believe is already under way—is one of a social system in chronic disrepair, for reasons of its own and regardless of the absence of a viable alternative. While we cannot know when and how exactly capitalism will disappear and what will succeed it, what matters is that no force is on hand that could be expected to reverse the three downward trends in economic growth, social equality and financial stability and end their mutual reinforcement. In contrast to the 1930s, there is today no political-economic formula on the horizon, left or right, that might provide capitalist societies with a coherent new regime of regulation, or régulation. Social integration as well as system integration seem irreversibly damaged and set to deteriorate further.footnote16 What is most likely to happen as time passes is a continuous accumulation of small and not-so-small dysfunctions; none necessarily deadly as such, but most beyond repair, all the more so as they become too many for individual address. In the process, the parts of the whole will fit together less and less; frictions of all kinds will multiply; unanticipated consequences will spread, along ever more obscure lines of causation. Uncertainty will proliferate; crises of every sort—of legitimacy, productivity or both—will follow each other in quick succession while predictability and governability will decline further (as they have for decades now). Eventually, the myriad provisional fixes devised for short-term crisis management will collapse under the weight of the daily disasters produced by a social order in profound, anomic disarray.

Conceiving of the end of capitalism as a process rather than an event raises the issue of how to define capitalism. Societies are complex entities that do not die in the way organisms do: with the rare exception of total extinction, discontinuity is always embedded in some continuity. If we say that a society has ended, we mean that certain features of its organization that we consider essential to it have disappeared; others may well have survived. I propose that to determine if capitalism is alive, dying or dead, we define it as a modern societyfootnote17 that secures its collective reproduction as an unintended side-effect of individually rational, competitive profit maximization in pursuit of capital accumulation, through a ‘labour process’ combining privately owned capital with commodified labour power, fulfilling the Mandevillean promise of private vices turning into public benefits.footnote18 It is this promise, I maintain, that contemporary capitalism can no longer keep—ending its historical existence as a self-reproducing, sustainable, predictable and legitimate social order.

The demise of capitalism so defined is unlikely to follow anyone’s blueprint. As the decay progresses, it is bound to provoke political protests and manifold attempts at collective intervention. But for a long time, these are likely to remain of the Luddite sort: local, dispersed, uncoordinated, ‘primitive’—adding to the disorder while unable to create a new order, at best unintentionally helping it to come about. One might think that a long-lasting crisis of this sort would open up more than a few windows of opportunity for reformist or revolutionary agency. It seems, however, that disorganized capitalism is disorganizing not only itself but its opposition as well, depriving it of the capacity either to defeat capitalism or to rescue it. For capitalism to end, then, it must provide for its own destruction—which, I would argue, is exactly what we are witnessing today.

A Pyrrhic victory

But why should capitalism, whatever its deficiencies, be in crisis at all if it no longer has any opposition worthy of the name? When communism imploded in 1989, this was widely viewed as capitalism’s final triumph, as the ‘end of history’. Even today, after 2008, the Old Left remains on the brink of extinction everywhere, while a new New Left has up to now failed to appear. The masses, the poor and powerless as much as the relatively well-to-do, seem firmly in the grip of consumerism, with collective goods, collective action and collective organization thoroughly out of fashion. As the only game in town, why should capitalism not carry on, by default if for no other reason? At first glance, there is indeed much that speaks against pronouncing capitalism dead, regardless of all the ominous writing on the historical wall. As far as inequality is concerned, people may get used to it, especially with the help of public entertainment and political repression. Furthermore, examples abound of governments being re-elected that cut social spending and privatize public services, in pursuit of sound money for the owners of money. Concerning environmental deterioration, it proceeds only slowly compared to the human lifespan, so one can deny it while learning to live with it. Technological advances with which to buy time, such as fracking, can never be ruled out, and if there are limits to the pacifying powers of consumerism, we clearly are nowhere near them. Moreover, adapting to more time-consuming and life-consuming work regimes can be taken as a competitive challenge, an opportunity for personal achievement. Cultural definitions of the good life have always been highly malleable and might well be stretched further to match the onward march of commodification, at least as long as radical or religious challenges to pro-capitalist re-education can be suppressed, ridiculed or otherwise marginalized. Finally, most of today’s stagnation theories apply only to the West, or just to the us, not to China, Russia, India or Brazil—countries to which the frontier of economic growth may be about to migrate, with vast virgin lands waiting to be made available for capitalist progress.footnote19

My answer is that having no opposition may actually be more of a liability for capitalism than an asset. Social systems thrive on internal heterogeneity, on a pluralism of organizing principles protecting them from dedicating themselves entirely to a single purpose, crowding out other goals that must also be attended to if the system is to be sustainable. Capitalism as we know it has benefited greatly from the rise of countermovements against the rule of profit and of the market. Socialism and trade unionism, by putting a brake on commodification, prevented capitalism from destroying its non-capitalist foundations—trust, good faith, altruism, solidarity within families and communities, and the like. Under Keynesianism and Fordism, capitalism’s more or less loyal opposition secured and helped stabilize aggregate demand, especially in recessions. Where circumstances were favourable, working-class organization even served as a ‘productivity whip’, by forcing capital to embark on more advanced production concepts. It is in this sense that Geoffrey Hodgson has argued that capitalism can survive only as long as it is not completely capitalist—as it has not yet rid itself, or the society in which it resides, of ‘necessary impurities’.footnote20 Seen this way, capitalism’s defeat of its opposition may actually have been a Pyrrhic victory, freeing it from countervailing powers which, while sometimes inconvenient, had in fact supported it. Could it be that victorious capitalism has become its own worst enemy?

Frontiers of commodification

In exploring this possibility, we might wish to turn to Karl Polanyi’s idea of social limits to market expansion, as underlying his concept of the three ‘fictitious commodities’: labour, land (or nature) and money.footnote21 A fictitious commodity is defined as a resource to which the laws of supply and demand apply only partially and awkwardly if at all; it can therefore only be treated as a commodity in a carefully circumscribed, regulated way, since complete commodification will destroy it or make it unusable. Markets, however, have an inherent tendency to expand beyond their original domain, the trading of material goods, to all other spheres of life, regardless of their suitability for commodification—or, in Marxian terms, for subsumption under the logic of capital accumulation. Unless held back by constraining institutions, market expansion is thus at permanent risk of undermining itself, and with it the viability of the capitalist economic and social system.

In fact, the indications are that market expansion has today reached a critical threshold with respect to all three of Polanyi’s fictitious commodities, as institutional safeguards that served to protect them from full marketization have been eroded on a number of fronts. This is what seems to be behind the search currently under way in all advanced capitalist societies for a new time regime with respect to labour, in particular a new allocation of time between social and economic relations and pursuits; for a sustainable energy regime in relation to nature; and for a stable financial regime for the production and allocation of money. In all three areas, societies are today groping for more effective limitations on the logic of expansion,footnote22 institutionalized as one of private enrichment, that is fundamental to the capitalist social order. These limitations centre on the increasingly demanding claims made by the employment system on human labour, by capitalist production and consumption systems on finite natural resources, and by the financial and banking system on people’s confidence in ever more complex pyramids of money, credit and debt.

Looking at each of the three Polanyian crisis zones in turn, we may note that it was an excessive commodification of money that brought down the global economy in 2008: the transformation of a limitless supply of cheap credit into ever more sophisticated financial ‘products’ gave rise to a real-estate bubble of a size unimaginable at the time. As of the 1980s, deregulation of us financial markets had abolished the restrictions on the private production and marketization of money devised after the Great Depression. ‘Financialization’, as the process came to be known, seemed the last remaining way to restore growth and profitability to the economy of the overextended hegemon of global capitalism. Once let loose, however, the money-making industry invested a good part of its enormous resources in lobbying for a further removal of prudential regulation, not to mention in circumventing whatever rules were left. With hindsight, the enormous risks that came with the move from the old regime of m–c–m´ to a new one of m–m´ are easy to see, as is the trend toward ever-increasing inequality associated with the disproportionate growth of the banking sector.footnote23

Concerning nature, there is growing unease over the tension, now widely perceived, between the capitalist principle of infinite expansion and the finite supply of natural resources. Neo-Malthusian discourses of various denominations became popular in the 1970s. Whatever one may think of them, and although some are now considered prematurely alarmist, no one seriously denies that the energy consumption patterns of rich capitalist societies cannot be extended to the rest of the world without destroying essential preconditions of human life. What seems to be taking shape is a race between the advancing exhaustion of nature on the one hand and technological innovation on the other—substituting artificial materials for natural ones, preventing or repairing environmental damage, devising shelters against unavoidable degradation of the biosphere. One question that no one seems able to answer is how the enormous collective resources potentially required for this may be mobilized in societies governed by what C. B. MacPherson termed ‘possessive individualism’.footnote24 What actors and institutions are to secure the collective good of a liveable environment in a world of competitive production and consumption?

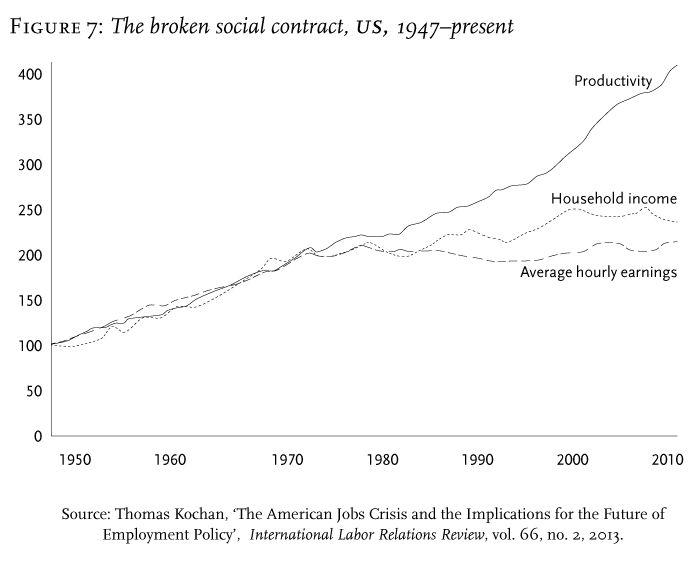

Thirdly, the commodification of human labour may have reached a critical point. Deregulation of labour markets under international competition has undone whatever prospects there might once have been for a general limitation of working hours.footnote25 It has also made employment more precarious for a growing share of the population.footnote26 With the rising labour-market participation of women, due in part to the disappearance of the ‘family wage’, hours per month sold by families to employers have increased while wages have lagged behind productivity, most dramatically in the capitalist heartland, the us (see Figure 7). At the same time, deregulation and the destruction of trade unions notwithstanding, labour markets typically fail to clear, and residual unemployment on the order of 7 to 8 per cent has become the new normal, even in a country like Sweden. Sweatshops have expanded in many industries including services, but mostly on the global periphery, beyond the reach of the authorities and what remains of trade unions in the capitalist centre, and out of view of consumers. As sweated labour competes with workers in countries with historically strong labour protections, working conditions for the former deteriorate while unemployment becomes endemic for the latter. Meanwhile, complaints multiply about the penetration of work into family life, alongside pressures from labour markets to join an unending race to upgrade one’s ‘human capital’. Moreover, global mobility enables employers to replace unwilling local workers with willing immigrant ones. It also compensates for sub-replacement fertility, itself due in part to a changed balance between unpaid and paid work and between non-market and market consumption. The result is a secular weakening of social counter-movements, caused by a loss of class and social solidarity and accompanied by crippling political conflicts over ethnic diversity, even in traditionally liberal countries such as the Netherlands, Sweden or Norway.

The question of how and where capital accumulation must be restrained in order to protect the three fictitious commodities from total commodification has been contested throughout the history of capitalism. But the present worldwide disorder in all three border zones at the same time is something different: it results from a spectacularly successful onslaught of markets, expanding more rapidly than ever, on a wide range of institutions and actors that, whether inherited from the past or built up in long political struggles, had for a time kept capitalism’s advance to some extent socially embedded. Labour, land and money have simultaneously become crisis zones after ‘globalization’ endowed market relations and production chains with an unprecedented capacity to cross the boundaries of national political and legal jurisdictions. The result is a fundamental disorganization of the agencies that have, in the modern era, more or less successfully domesticated capitalist ‘animal spirits’, for the sake of society as a whole as well as of capitalism itself.

It is not only with respect to fictitious commodities that capital accumulation may be hitting its limits. On the surface, consumption of goods and services continues to grow, and the implicit premise of modern economics—that the human desire and capacity to consume are unlimited—would seem to be easily vindicated by a visit to any large shopping mall. Still, fears that markets for consumer goods may at some point become saturated—perhaps in the course of a post-materialist decoupling of human aspirations from the purchase of commodities—are endemic among profit-dependent producers. This in itself reflects the fact that consumption in mature capitalist societies has long become dissociated from material need.footnote27 The lion’s share of consumption expenditure today—and a rapidly growing one—is spent not on the use value of goods, but on their symbolic value, their aura or halo. This is why industry practitioners find themselves paying more than ever for marketing, including not just advertising but also product design and innovation. Nevertheless, in spite of the growing sophistication of sales promotion, the intangibles of culture make commercial success difficult to predict—certainly more so than in an era when growth could be achieved by gradually supplying all households in a country with a washing machine.footnote28

Five disorders

Capitalism without opposition is left to its own devices, which do not include self-restraint. The capitalist pursuit of profit is open-ended, and cannot be otherwise. The idea that less could be more is not a principle a capitalist society could honour; it must be imposed upon it, or else there will be no end to its progress, self-consuming as it may ultimately be. At present, I claim, we are already in a position to observe capitalism passing away as a result of having destroyed its opposition—dying, as it were, from an overdose of itself. For illustration I will point to five systemic disorders of today’s advanced capitalism; all of them result in various ways from the weakening of traditional institutional and political restraints on capitalist advance. I call them stagnation, oligarchic redistribution, the plundering of the public domain, corruption and global anarchy.

Six years after Lehman, predictions of long-lasting economic stagnation are en vogue. A prominent example is a much-discussed paper by Robert Gordon, who argues that the main innovations that have driven productivity and economic growth since the 1800s could happen only once, like the increase in the speed of transportation or the installation of running water in cities.footnote29 Compared to them, the recent spread of information technology has produced only minor productivity effects, if any. While Gordon’s argument may seem somewhat technologically deterministic, it appears plausible that capitalism can hope to attain the level of growth needed to compensate a non-capitalist working class for helping others accumulate capital only if technology opens up ever new opportunities for increasing productivity. In any case, in what looks like an afterthought Gordon supports his prediction of low or no growth by listing six non-technological factors—he calls them ‘headwinds’—which would make for long-term stagnation ‘even if innovation were to continue . . . at the rate of the two decades before 2007’.footnote30 Among these factors he includes two that I argue have for some time been intertwined with low growth: inequality and ‘the overhang of consumer and government debt’.footnote31

What is astonishing is how close current stagnation theories come to the Marxist underconsumption theories of the 1970s and 1980s.footnote32 Recently, none other than Lawrence ‘Larry’ Summers—friend of Wall Street, chief architect of financial deregulation under Clinton, and Obama’s first choice for president of the Federal Reserve, until he had to give way in face of congressional oppositionfootnote33—has joined the stagnation theorists. At the imf Economic Forum on November 8 last year, Summers confessed to having given up hope that close-to-zero interest rates would produce significant economic growth in the foreseeable future, in a world he felt was suffering from an excess of capital.footnote34 Summers’ prediction of ‘secular stagnation’ as the ‘new normal’ met with surprisingly broad approval among his fellow economists, including Paul Krugman.footnote35 What Summers mentioned only in passing was that the conspicuous failure of even negative real interest rates to revive investment coincided with a long-term increase in inequality, in the us and elsewhere. As Keynes would have known, concentration of income at the top must detract from effective demand and make capital owners look for speculative profit opportunities outside the ‘real economy’. This may in fact have been one of the causes of the ‘financialization’ of capitalism that began in the 1980s.

The power elites of global capitalism would seem to be resigning themselves to low or no growth on aggregate for the foreseeable future. This does not preclude high profits in the financial sector, essentially from speculative trading with cheap money supplied by central banks. Few seem to fear that the money generated to prevent stagnation from turning into deflation will cause inflation, as the unions that could claim a share in it no longer exist.footnote36 In fact the concern now is with too little rather than too much inflation, the emerging received wisdom being that a healthy economy requires a yearly inflation rate of at least 2 per cent, if not more. The only inflation in sight, however, is that of asset-price bubbles, and Summers took pains to prepare his audience for a lot of them.

For capitalists and their retainers, the future looks like a decidedly bumpy ride. Low growth will refuse them additional resources with which to settle distributional conflicts and pacify discontent. Bubbles are waiting to burst, out of the blue, and it is not certain whether states will regain the capacity to take care of the victims in time. The stagnant economy that is shaping up will be far from a stationary or steady-state economy; as growth declines and risks increase, the struggle for survival will become more intense. Rather than restoring the protective limits to commodification that were rendered obsolete by globalization, ever new ways will be sought to exploit nature, extend and intensify working time, and encourage what the jargon calls creative finance, in a desperate effort to keep profits up and capital accumulation going. The scenario of ‘stagnation with a chance of bubbles’ may most plausibly be imagined as a battle of all against all, punctured by occasional panics and with the playing of endgames becoming a popular pastime.

Plutocrats and plunder

Turning to the second disorder, there is no indication that the long-term trend towards greater economic inequality will be broken any time soon, or indeed ever. Inequality depresses growth, for Keynesian and other reasons. But the easy money currently provided by central banks to restore growth—easy for capital but not, of course, for labour—further adds to inequality, by blowing up the financial sector and inviting speculative rather than productive investment. Redistribution to the top thus becomes oligarchic: rather than serving a collective interest in economic progress, as promised by neoclassical economics, it turns into extraction of resources from increasingly impoverished, declining societies. Countries that come to mind here are Russia and Ukraine, but also Greece and Spain, and increasingly the United States. Under oligarchic redistribution, the Keynesian bond which tied the profits of the rich to the wages of the poor is severed, cutting the fate of economic elites loose from that of the masses.footnote37 This was anticipated in the infamous ‘plutonomy’ memorandums distributed by Citibank in 2005 and 2006 to a select circle of its richest clients, to assure them that their prosperity no longer depended on that of wage earners.footnote38

Oligarchic redistribution and the trend toward plutonomy, even in countries that are still considered democracies, conjure up the nightmare of elites confident that they will outlive the social system that is making them rich. Plutonomic capitalists may no longer have to worry about national economic growth because their transnational fortunes grow without it; hence the exit of the super-rich from countries like Russia or Greece, who take their money—or that of their fellow-citizens—and run, preferably to Switzerland, Britain or the United States. The possibility, as provided by a global capital market, of rescuing yourself and your family by exiting together with your possessions offers the strongest possible temptation for the rich to move into endgame mode—cash in, burn bridges, and leave nothing behind but scorched earth.

Closely related to this is the third disorder, the plundering of the public domain through underfunding and privatization. I have elsewhere traced its origin to the twofold transition since the 1970s from the tax state to the debt state to, finally, the consolidation or austerity state. Foremost among the causes of this shift were the new opportunities offered by global capital markets since the 1980s for tax flight, tax evasion, tax-regime shopping, and the extortion of tax cuts from governments by corporations and earners of high incomes. Attempts to close public deficits relied almost exclusively on cuts in government spending—both to social security and to investment in physical infrastructures and human capital. As income gains accrued increasingly to the top one per cent, the public domain of capitalist economies shrank, often dramatically, starved in favour of internationally mobile oligarchic wealth. Part of the process was privatization, carried out regardless of the contribution public investment in productivity and social cohesion might have made to economic growth and social equity.

Even before 2008, it was generally taken for granted that the fiscal crisis of the postwar state had to be resolved by lowering spending instead of raising taxes, especially on the rich. Consolidation of public finances by way of austerity was and is being imposed on societies even though it is likely to depress growth. This would seem to be another indication that the economy of the oligarchs has been decoupled from that of ordinary people, as the rich no longer expect to pay a price for maximizing their income at the expense of the non-rich, or for pursuing their interests at the expense of the economy as a whole. What may be surfacing here is the fundamental tension described by Marx between, on the one hand, the increasingly social nature of production in an advanced economy and society, and private ownership of the means of production on the other. As productivity growth requires more public provision, it tends to become incompatible with private accumulation of profits, forcing capitalist elites to choose between the two. The result is what we are seeing already today: economic stagnation combined with oligarchic redistribution.footnote39

Corrosions of the iron cage

Along with declining economic growth, rising inequality and the transferral of the public domain to private ownership, corruption is the fourth disorder of contemporary capitalism. In his attempt to rehabilitate it by reclaiming its ethical foundations, Max Weber drew a sharp line between capitalism and greed, pointing to what he believed were its origins in the religious tradition of Protestantism. According to Weber, greed had existed everywhere and at all times; not only was it not distinctive of capitalism, it was even apt to subvert it. Capitalism was based not on a desire to get rich, but on self-discipline, methodical effort, responsible stewardship, sober devotion to a calling and to a rational organization of life. Weber did expect the cultural values of capitalism to fade as it matured and turned into an ‘iron cage’, where bureaucratic regulation and the constraints of competition would take the place of the cultural ideas that had originally served to disconnect capital accumulation from both hedonistic-materialistic consumption and primitive hoarding instincts. What he could not anticipate, however, was the neoliberal revolution in the last third of the twentieth century and the unprecedented opportunities it provided to get very rich.

Pace Weber, fraud and corruption have forever been companions of capitalism. But there are good reasons to believe that with the rise of the financial sector to economic dominance, they have become so pervasive that Weber’s ethical vindication of capitalism now seems to apply to an altogether different world. Finance is an ‘industry’ where innovation is hard to distinguish from rule-bending or rule-breaking; where the payoffs from semi-legal and illegal activities are particularly high; where the gradient in expertise and pay between firms and regulatory authorities is extreme; where revolving doors between the two offer unending possibilities for subtle and not-so-subtle corruption;footnote40 where the largest firms are not just too big to fail, but also too big to jail, given their importance for national economic policy and tax revenue; and where the borderline between private companies and the state is more blurred than anywhere else, as indicated by the 2008 bailout or by the huge number of former and future employees of financial firms in the American government. After Enron and WorldCom, it was observed that fraud and corruption had reached all-time highs in the us economy. But what came to light after 2008 beat everything: rating agencies being paid by the producers of toxic securities to award them top grades; offshore shadow banking, money laundering and assistance in large-scale tax evasion as the normal business of the biggest banks with the best addresses; the sale to unsuspecting customers of securities constructed so that other customers could bet against them; the leading banks worldwide fraudulently fixing interest rates and the gold price, and so on. In recent years, several large banks have had to pay billions of dollars in fines for activities of this sort, and more developments of this kind seem to be in the offing. What at first glance may look like quite significant sanctions, however, appear minuscule when compared to the banks’ balance sheets—not to mention the fact that all of these were out-of-court settlements of cases that governments didn’t want or dare to prosecute.footnote41

Capitalism’s moral decline may have to do with its economic decline, the struggle for the last remaining profit opportunities becoming uglier by the day and turning into asset-stripping on a truly gigantic scale. However that may be, public perceptions of capitalism are now deeply cynical, the whole system commonly perceived as a world of dirty tricks for ensuring the further enrichment of the already rich. Nobody believes any more in a moral revival of capitalism. The Weberian attempt to prevent it from being confounded with greed has finally failed, as it has more than ever become synonymous with corruption.

A world out of joint

We come, finally, to the fifth disorder. Global capitalism needs a centre to secure its periphery and provide it with a credible monetary regime. Until the 1920s, this role was performed by Britain, and from 1945 until the 1970s by the United States; the years in between, when a centre was missing, and different powers aspired to take on the role, were a time of chaos, economically as well as politically. Stable relations between the currencies of the countries participating in the capitalist world economy are essential for trade and capital flows across national borders, which are in turn essential for capital accumulation; they need to be underwritten by a global banker of last resort. An effective centre is also required to support regimes on the periphery willing to condone the low-price extraction of raw materials. Moreover, local collaboration is needed to hold down traditionalist opposition to capitalist Landnahme outside the developed world.

Contemporary capitalism increasingly suffers from global anarchy, as the United States is no longer able to serve in its postwar role, and a multipolar world order is nowhere on the horizon. While there are (still?) no great-power clashes, the dollar’s function as international reserve currency is contested—and cannot be otherwise, given the declining performance of the American economy, its rising levels of public and private debt, and the recent experience of several highly destructive financial crises. The search for an international alternative, perhaps in the form of a currency basket, is getting nowhere since the us cannot afford to give up the privilege of indebting itself in its own currency. Moreover, stabilizing measures taken by international organizations at Washington’s behest have increasingly tended to have destabilizing effects on the periphery of the system, as in the case of the inflationary bubbles caused in countries like Brazil and Turkey by ‘quantitative easing’ in the centre.

Militarily, the us has now been either defeated or deadlocked in three major land wars since the 1970s, and will in future probably be more reluctant to intervene in local conflicts with ‘boots on the ground’. New, sophisticated means of violence are being deployed to reassure collaborating governments and inspire confidence in the us as a global enforcer of oligarchic property rights, and as a safe haven for oligarchic families and their treasure. They include the use of highly secretive ‘special forces’ to seek out potential enemies for individualized destruction; unmanned aircraft capable of killing anybody at almost any place on the globe; confinement and torture of unknown numbers of people in a worldwide system of secret prison camps; and comprehensive surveillance of potential opposition everywhere with the help of ‘big data’ technology. Whether this will be enough to restore global order, especially in light of China’s rise as an effective economic and, to a lesser extent, military rival to the us may, however, be doubted.

In summary, capitalism, as a social order held together by a promise of boundless collective progress, is in critical condition. Growth is giving way to secular stagnation; what economic progress remains is less and less shared; and confidence in the capitalist money economy is leveraged on a rising mountain of promises that are ever less likely to be kept. Since the 1970s, the capitalist centre has undergone three successive crises, of inflation, public finances and private debt. Today, in an uneasy phase of transition, its survival depends on central banks providing it with unlimited synthetic liquidity. Step by step, capitalism’s shotgun marriage with democracy since 1945 is breaking up. On the three frontiers of commodification—labour, nature and money—regulatory institutions restraining the advance of capitalism for its own good have collapsed, and after the final victory of capitalism over its enemies no political agency capable of rebuilding them is in sight. The capitalist system is at present stricken with at least five worsening disorders for which no cure is at hand: declining growth, oligarchy, starvation of the public sphere, corruption and international anarchy. What is to be expected, on the basis of capitalism’s recent historical record, is a long and painful period of cumulative decay: of intensifying frictions, of fragility and uncertainty, and of a steady succession of ‘normal accidents’—not necessarily but quite possibly on the scale of the global breakdown of the 1930s.